Call Today

(971) 231 - 2400

Waiting on your Employee Retention Credit (ERC) refund? Learn how ERC advances work, the pros & cons, and if selling your credit for upfront cash is right for your business.

The Employee Retention Credit (ERC) has become a major financial relief program for businesses and nonprofits that were impacted by the COVID-19 pandemic. Some employers may consider an ERC Advance or advance, where a third party purchases the ERC claim for immediate cash.

So, what is an ERC advance, how does it work, and more importantly, is it the right move for your organization? This guide breaks down the process, outlines the pros and cons, details the required documentation, and helps you decide if an ERC advance fits your financial goals.

The Employee Retention Credit (ERC) is a refundable tax credit to support organizations that kept employees and were affected during COVID-19 pandemic in 2020 and 2021. Eligible employers could claim up to $26,000 per employee paid via check. However, processing delays have led to refunds taking 12–18 months or even longer.

This is where an Employee Retention Credit advance becomes helpful. It gives employers access to funds upfront instead of waiting for IRS processing. For many employers, the uncertainty around ERC refunds makes it feel too risky to keep waiting, so securing cash now offers greater peace of mind and control.

An ERC Advance allows you to sell your pending ERC refund to a purchasing fund. In exchange, you receive a lump sum payment upfront—usually 70% to 90% of your total claim. The buyer then collects the full refund from the IRS when it’s processed.

Think of it as trading future money for immediate capital.

Here’s why many businesses are turning to this strategy:

The ERC advance process requires understanding for anyone who wants to sell their ERC refund. The basic idea of getting immediate cash instead of waiting for IRS payment remains straightforward but the process requires multiple verification steps to safeguard both parties.

Buyers will review your filing, financials, and documentation before making an offer.

Once everything checks out, the process often finishes within a few weeks.

Here’s a simple overview of the typical process:

To qualify for an ERC advance, ERC Buyout or ERC loan, businesses typically need to submit the following documentation for underwriting and eligibility review:

Having your documents ready ahead of time helps speed up approval and ensures you receive a fair, accurate offer from potential buyers.

Before you sell ERC tax credits, consider the potential downsides:

It is advisable to thoroughly review your ERC claims and know the potential risks in advance to ensure that you have a clear understanding of your eligibility before proceeding with the sale.

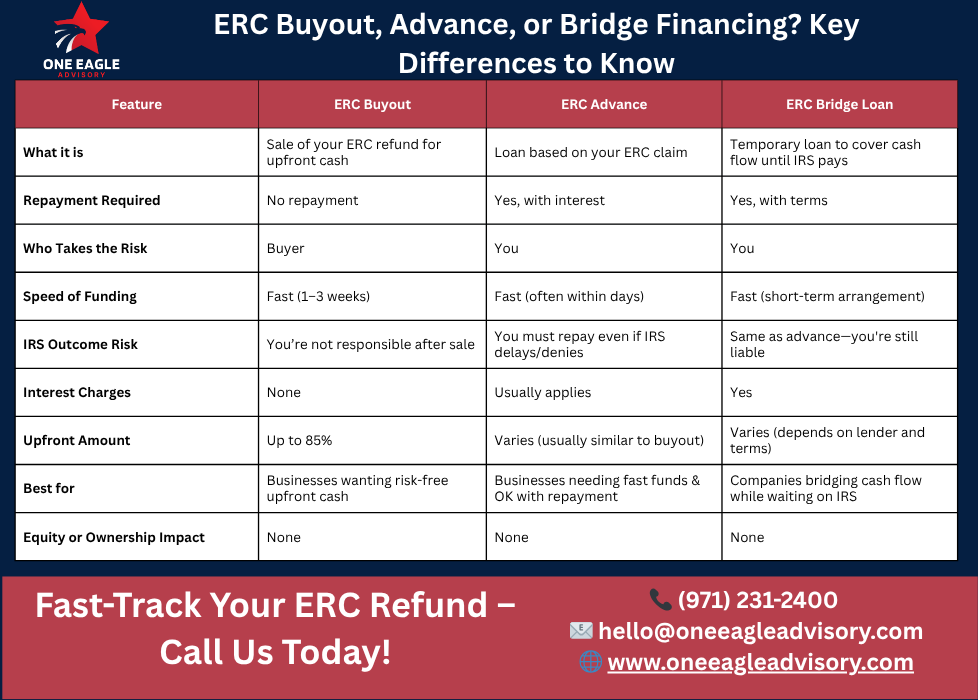

The ERC refund process leads many applicants to explore three funding alternatives which include an ERC buyout, ERC advance or ERC bridge financing. While they all help you access cash upfront, they work in very different ways.

How do you decide? If your main goal is speed and simplicity without risk, an ERC buyout is likely the better choice. But if you're okay with taking on some repayment responsibility in exchange for a bit more flexibility or potentially a higher advance, then an ERC advance or bridge loan might be a good fit.

Below is a quick breakdown to help you understand what’s best for your business:

Before saying yes to an Employee Retention Credit advance, it’s a good idea to think through a few important things. A thoughtful approach can help you make the right call for your business.

Ask yourself:

You don’t have to sell your entire ERC refund. You can actually choose to sell just a portion of it. This way, you get some quick cash to boost your business now while still keeping the rest of your refund to receive later. It’s a great middle-ground if you need funds but don’t want to give up your full refund.

We make ERC advances, ERC buyouts, and ERC bridge financing easy, fast, and secure. Our team specializes in helping businesses unlock the full value of their Employee Retention Credit through flexible funding solutions tailored to your needs.

Here’s what sets us apart:

Getting an Employee Retention Credit advance or selling your ERC credits doesn’t have to be complicated. Our team is here to ensure a seamless and secure experience.

Selling your ERC credit through an ERC advance or ERC buyout may be the right financial move if you need capital now and can’t wait any longer. While you won’t receive the full amount, getting your ERC refund today can help sustain or grow your business. ERC advance isn’t just about faster cash, it’s about putting your refund to work when it matters most. If timing is everything in business, this could be the right move to keep yours moving forward.

It’s important to carefully evaluate both the advantages and potential drawbacks of an ERC advance and consider how it may impact your business in the long term. Speaking with a financial advisor or tax professional can help you make a well-informed decision that supports your overall financial strategy.

And, if you're considering an ERC credit loan, an ERC credit advance, or want to sell ERC credits outright, we’re here to guide you. We’ll help you understand your options and choose the best solution for your business needs. We’re here to give you the support, clarity and confidence you need to make the most of your ERC refund.

Still have questions? Check out our ERC advance FAQs

.png)

.png)